You bought a 22K set during Akshaya Tritiya, inherited coins from your grandmother, or hold paper gold in a demat account. Each path crosses a different tax line — GST at purchase, capital gains at sale, and sometimes TDS at the counter. Gujarat buyers who treat every piece as "tax-free gold" often get surprised at filing season. This guide maps how gold is taxed in India by product type and transaction, without repeating buy-back mechanics covered elsewhere.

For how jewellers calculate scrap payouts, see our sell old gold guide — one sentence only: that article covers counter math, not IT rules. For Sovereign Gold Bond maturity exemption, see our SGB vs physical gold guide. Check today's gold price today on GS24Live for market context.

Key Takeaways

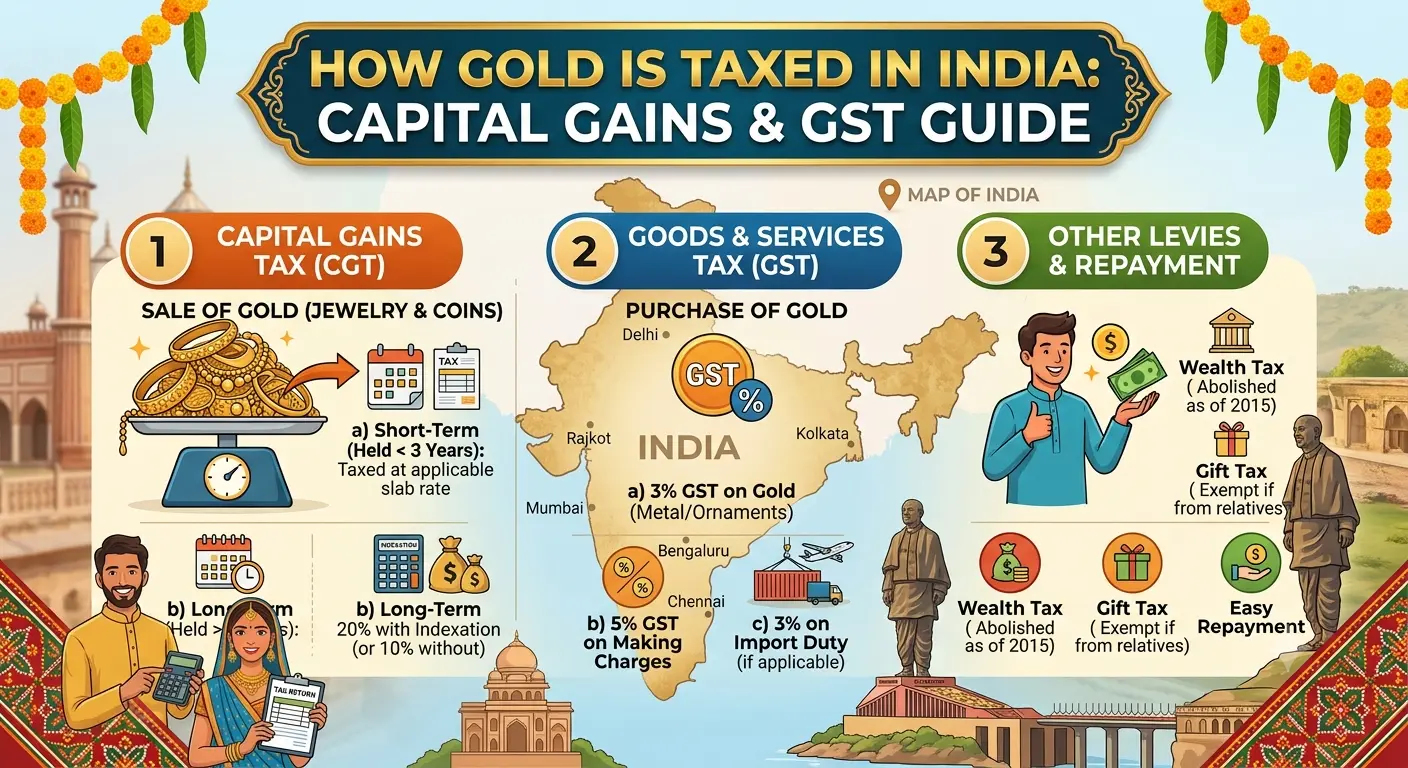

- GST applies when you buy new jewellery (3% on gold value plus making charges in most retail structures) — it is not automatically refunded when you sell old scrap.

- Physical gold sales may trigger capital gains tax depending on holding period and purchase documentation — short-term and long-term rates differ.

- Sovereign Gold Bonds carry a distinct tax treatment at maturity — see the dedicated SGB article rather than assuming physical-gold rules apply.

- Gold ETFs and digital gold follow securities or contract tax paths — not identical to selling a bangle at a saraf.

- Keep purchase invoices, bank proofs, and SGB certificates — Gujarat families with records file cleaner returns and face fewer scrutiny delays.

GST When You Buy Gold Jewellery

Retail jewellery invoices typically show gold value, making charges, and GST components separately. The tax is embedded in what you pay at the counter — it does not increase your metal weight. When you later sell scrap, the buyer pays for metal content at buy-back rates; GST paid years ago is generally not returned as a separate line item.

| Invoice line | Typical tax treatment (retail) | Resale implication |

|---|---|---|

| Gold value (22K/24K) | 3% GST on value portion | Not recovered at scrap sale |

| Making charges | 3% or 5% depending on structure | Making not paid back at buy-back |

| Coins/bars (specified units) | May differ from jewellery billing | Check invoice category at purchase |

Capital Gains on Physical Gold Sales

When you sell physical gold — jewellery, coins, bars — for more than your cost basis, the profit may be taxable as capital gains. Classification depends on how long you held the asset and whether you can prove acquisition cost. Rules evolve with Finance Acts — verify the current year's thresholds with a chartered accountant before filing.

| Scenario | Typical holding lens | Tax treatment (general framework) |

|---|---|---|

| Short-term sale | Held up to statutory short-term period | May be taxed at slab rates applicable to you |

| Long-term sale | Held beyond long-term threshold | May qualify for long-term capital gains rate with indexation where applicable |

| Sale without purchase proof | Inherited or gifted long ago | Special valuation rules may apply — documentation critical |

| Jewellery vs investment coin | Same metal, different use | Tax character follows asset type and holding proof |

Tax by Gold Product Type

Not every gold exposure shares the same tax path. Treating ETF units like a physical chain sale is a common filing mistake.

| Product | Purchase tax | Sale / maturity tax (framework) |

|---|---|---|

| 22K jewellery | GST on invoice | Capital gains if profit on documented cost |

| Gold ETF (demat) | Brokerage; no GST like jewellery | Securities capital gains rules |

| Digital gold app | Platform-specific | Depends on product structure — read terms |

| Sovereign Gold Bond | No GST like jewellery | Interest taxable; maturity treatment distinct — see SGB guide |

| Gold mutual fund | Fund structure | Fund redemption tax rules apply |

For ETF mechanics, see our gold ETF guide — one sentence only. For digital gold vs mutual funds, see the mutual funds vs digital gold guide.

TDS and Large Cash Settlements

Certain gold sales above specified thresholds may attract tax deducted at source when buyers are obligated to withhold. Cash-heavy scrap deals without receipts create both tax reporting gaps and TDS ambiguity. Prefer traceable bank transfers and insist on a sale receipt with weight, rate, and buyer identification — especially on CG Road and Manek Chowk transactions above routine household size.

Inherited and Gifted Gold: Documentation Matters

Gold received by inheritance or gift carries acquisition cost and holding-period rules that differ from a piece you bought with a fresh invoice. Family settlements in Gujarat often lack paper trail — that makes fair-market valuation at sale or partition more complex. Photograph HUID tags, store prior invoices even if faded, and note the date of inheritance in your records folder.

Historical Tax Milestones for Gold in India

| Year / reform | What changed | Buyer impact |

|---|---|---|

| GST rollout (2017) | Unified indirect tax on jewellery purchases | Transparent invoice lines; no scrap GST refund |

| Finance Act updates (periodic) | Capital gains thresholds and rates adjusted | Verify current year before selling large lots |

| SGB programme expansion | Distinct maturity tax treatment vs physical | Investors must separate SGB certificates from jewellery folder |

| Increased digital reporting | More TDS and statement matching | Bank transfers and receipts reduce mismatch notices |

Gujarat Filing Habits: Ahmedabad CAs and Family Records

Gujarat's bullion-heavy households often hold gold for decades before a single large sale — wedding upgrades, business liquidity, or NR remittance events. Ahmedabad chartered accountants report cleaner filings when clients deliver a simple folder: purchase invoices, HUID photos, bank credit slips from scrap sales, and SGB demat statements kept separate from jewellery bills.

- After selling at Manek Chowk, email yourself the weight slip photo the same day — memory fades before July filing season.

- If you bought on Akshaya Tritiya annually, tag each invoice by year in a Google Drive folder; holding-period math becomes trivial.

- Surat and Rajkot business families mixing showroom purchases with import allocations should keep customs and GST documents distinct from retail counter bills.

Risks of Under-Reporting Gold Sale Proceeds

Informal cash scrap sales without receipts invite mismatch if bank deposits later exceed explained income. Claiming zero cost on inherited pieces without valuation support fails scrutiny. Mixing personal jewellery sales with undisclosed business inventory distorts GST and income tax positions simultaneously — a double exposure.

Practical Record-Keeping Strategy Before You Sell

- Collect every purchase invoice before listing scrap for sale — cost basis starts here.

- Sell with traceable payment and a receipt showing weight, purity, rate, and buyer GSTIN where applicable.

- Separate SGB, ETF, and physical folders — tax paths differ.

- Consult a CA before selling a large inherited lot — valuation rules may save tax legally.

- Do not assume making charges or GST return at buy-back — they do not.

Frequently Asked Questions

1. Do I pay GST again when selling old gold jewellery?

Scrap sales are generally not charged GST to you as a household seller the way retail purchases are. GST paid at original purchase is not refunded as a separate rebate when you sell — you receive buy-back value on metal content.

2. How is capital gains tax calculated on gold jewellery?

Tax applies on profit between documented acquisition cost (or permitted valuation) and sale proceeds, classified by holding period. Rates and indexation depend on current law — confirm with a tax professional for your filing year.

3. Is gold ETF taxation the same as selling physical gold?

No. Gold ETFs are securities held in demat form and follow capital gains rules for listed securities, not the same path as selling a bangle at a saraf counter.

4. Are Sovereign Gold Bond returns tax-free?

SGBs have distinct rules: periodic interest is taxable, and maturity redemption has a separate treatment from physical gold sales. See our dedicated SGB guide for the full framework — do not assume jewellery rules apply.

5. What if I sell gold without the original invoice?

You may still sell, but proving acquisition cost becomes harder. Inherited gold may use permitted valuation methods — documentation gaps increase audit friction and can affect computed gain.

6. Does TDS apply when I sell gold to a jeweller in Gujarat?

TDS obligations depend on transaction size, buyer type, and current statutory thresholds. Ask for a written statement if TDS is deducted and keep the certificate for filing.

Data Sources and References

- Reserve Bank of India (RBI) — Sovereign Gold Bond programme and RBI circular context.

- International Monetary Fund (IMF) — inflation and macro context for holding real assets.

- World Gold Council — Indian gold demand and investment behaviour.

- Reuters — market and policy news affecting bullion investors.

- Bureau of Indian Standards (BIS) — purity documentation supporting cost and sale records.

Conclusion

Tax on gold in India splits by product and transaction: GST hits at jewellery purchase, capital gains may apply at profitable sale, and SGBs plus ETFs follow their own paths. Gujarat buyers who keep invoices, HUID photos, and bank receipts file cleaner returns and avoid turning a fair scrap sale into a tax-season dispute.

Before your next sale, sort physical, ETF, and SGB holdings into separate folders and confirm the current year's rules with a qualified CA — metal value and tax liability are related but not identical numbers.

Disclaimer: This article is for informational and educational purposes only. Tax laws change frequently. Verify current rules with a qualified chartered accountant or tax professional before selling or filing.

Keywords: tax on gold India, gold capital gains tax, GST on gold jewellery, gold selling tax rules, SGB tax exemption, gold ETF taxation, TDS on gold sale Gujarat.