Indian households hold thousands of tonnes of gold in lockers and godrej almirahs — metal that earns nothing while inflation quietly erodes purchasing power. The Gold Monetisation Scheme (GMS), launched by the government and administered through banks and refineries, offers a regulated path to deposit idle bullion and earn interest without melting family jewellery for scrap. It is not a loan, not a bond, and not a showroom exchange offer — and misunderstanding that difference leads to rejected deposits and wasted trips.

This guide explains how the gold monetisation scheme in India works in 2026: deposit types, assay steps, interest bands, tax treatment, and when GMS beats keeping coins in a bank locker. For urgent rupee liquidity against pledged metal, see our gold loan Gujarat guide in one sentence only — loans advance cash against collateral; GMS pays you to hold refined gold with the bank. For tax on interest and sale, link to the gold tax guide. Check today's gold price today before you value your holding.

Key Takeaways

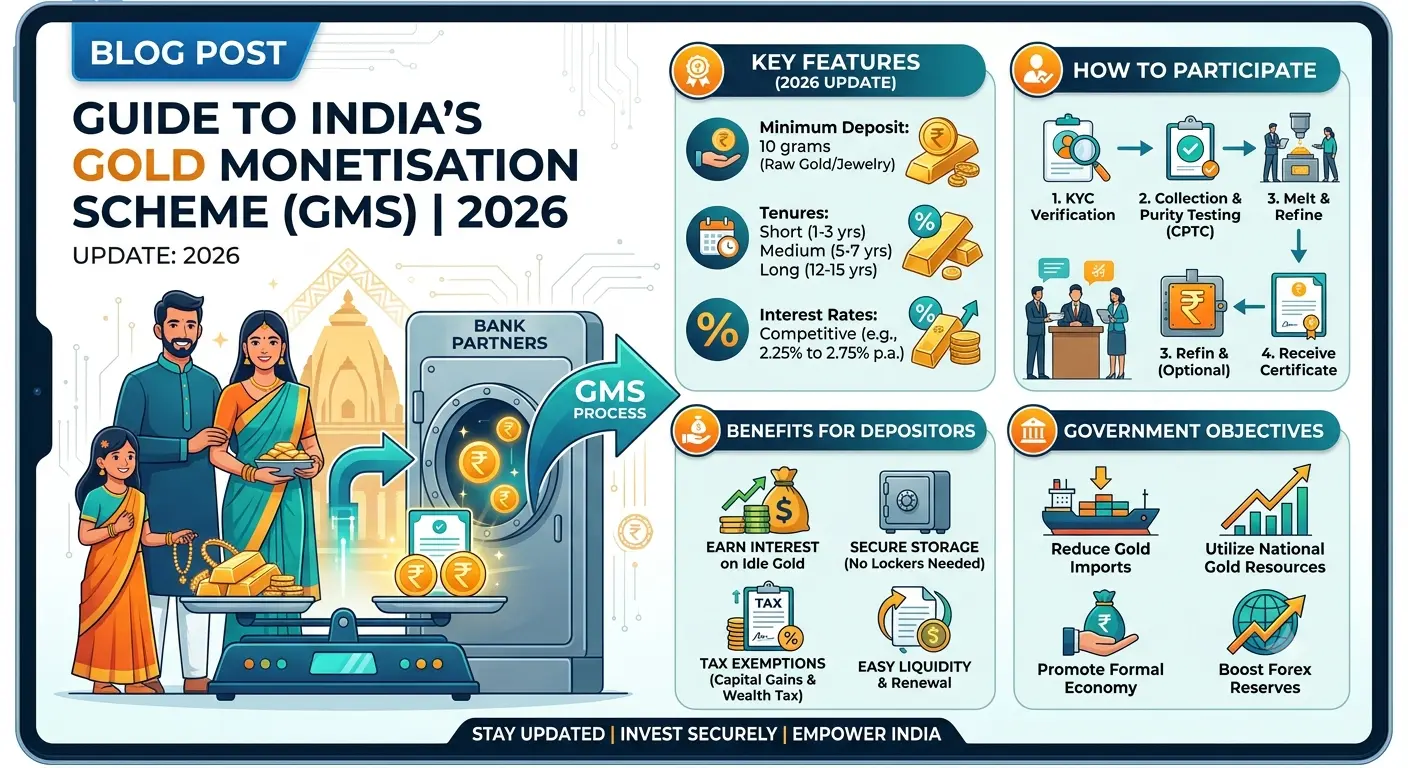

- GMS converts assayed gold into a deposit account paying interest — you do not sell ownership; you transfer refined metal into the scheme for a fixed term.

- Short-term deposits run one to three years; long-term deposits run five to seven years with typically higher interest bands.

- Minimum deposit thresholds and purity requirements apply — jewellery may need melting and refining; coins and bars are simpler.

- Interest is taxable; principal returns as gold of equivalent fineness at maturity subject to scheme rules — verify current RBI and bank circulars.

- Participation remains low because families resist melting heirloom designs — GMS suits idle bars and coins more than bridal sets.

What the Gold Monetisation Scheme Is

The Gold Monetisation Scheme pools domestically idle gold into the formal financial system. Banks act as intermediaries; refineries assay purity and melt acceptable lots. Depositors receive a Gold Deposit Certificate and earn interest denominated in gold or rupees per product terms. The objective is reducing physical gold imports by recycling metal already inside India — not replacing wedding jewellery culture.

GMS differs from Sovereign Gold Bonds, which are paper instruments with a sovereign coupon. For SGB mechanics, see our SGB vs physical gold guide in one sentence only. GMS also differs from selling scrap — for open-market sale math see the sell old gold guide.

Short-Term vs Long-Term GMS Deposits Compared

| Feature | Short-term deposit (STGD) | Long-term deposit (LTGD) |

|---|---|---|

| Tenure | 1–3 years (product-dependent) | 5–7 years (product-dependent) |

| Interest band (illustrative) | Lower — check live bank circular | Higher — compensates longer lock-in |

| Early withdrawal | Stricter rules; penalties may apply | Typically stricter than STGD |

| Best suited for | Idle coins/bars you may redeploy mid-term | Generational bars with no wear use |

| Jewellery with stones | Usually must melt — stone value separate | Same assay requirement |

Step-by-Step: From Locker to Interest Credit

- Collection centre visit: Approach a participating bank branch or designated refinery collection point with your gold and KYC documents.

- Preliminary test: Purity screening — non-hallmarked or below-minimum fineness may be rejected or priced down.

- Melting and assay: Acceptable lots are melted; final fineness determines credited grams.

- Deposit election: Choose STGD or LTGD; sign terms covering interest rate, tenure, and maturity redemption form.

- Certificate issue: Gold Deposit Certificate records grams credited — store with your bank locker agreement copies.

- Interest payout: Credited per schedule — confirm whether interest compounds or pays out periodically.

Worked Example: 100 Grams of 24K Bars (Illustrative)

| Line | Sample figure | Notes |

|---|---|---|

| Raw holding | 100g 24K bars | Bank or refinery hallmarked |

| Assay loss (sample 0.5%) | 99.5g credited | Melt and assay shrinkage varies |

| Metal value at ₹10,000/g (sample) | ₹9,95,000 reference | Not cash paid — gold remains in scheme |

| LTGD interest (2.25% p.a. sample) | ~2.24g/year gold-denominated interest | Verify live rate at deposit |

| Tax on interest | Taxable per Income Tax rules | See gold tax guide — link only |

| Locker cost avoided (5 yr sample) | ₹15,000–₹30,000 saved vs bank locker rent | Varies by branch and city |

GMS Milestones and Uptake in India

| Period | Policy / market note | Household impact |

|---|---|---|

| 1999 (predecessor) | Gold Deposit Scheme era | Limited retail awareness; bank-led |

| 2015 launch | GMS introduced with STGD/LTGD structure | Refinery pipeline formalised; low festive uptake |

| 2017–2020 | Banks expand collection tie-ups | Still dominated by institutions, not bridal lockers |

| 2021–2026 | High gold prices raise opportunity cost of idle metal | Renewed interest in coins/bars; jewellery melting resistance persists |

Ahmedabad & Gujarat: Collection Centres and Local Behaviour

Gujarat's gold culture centres on wearable jewellery and merchant-family bars — not idle London Good Delivery bricks. Ahmedabad participants typically approach scheduled commercial bank branches advertising GMS tie-ins rather than neighbourhood scrap lanes. Surat and Rajkot wholesale families with refinery relationships may route large bar lots through assay channels faster than first-time retail depositors.

- Call the branch two days before carrying metal — not every CG Road showroom bank counter accepts melt deposits daily.

- Separate sentimental jewellery from deposit candidates before travel; once melted, the design is gone even if you redeem metal later.

- Compare GMS interest plus avoided locker rent against a gold loan only if you need cash flow — different problem.

- Keep assay receipts and the Gold Deposit Certificate in the same folder as original purchase invoices for tax continuity.

Risks: Purity Disputes, Melting Heirlooms, and Low Liquidity

GMS is illiquid compared to a locker withdrawal. Early exit may cost penalties or be unavailable on LTGD. Assay results below your expectation — common with old 22K mixed lots — reduce credited grams. Heirloom jewellery loses craft value the moment it enters the melt pot; GMS is financially rational only when craft value is already irrelevant to you.

Scheme participation and interest rates depend on bank appetite and government notification — terms that held in 2024 may differ in 2026. Never assume a cousin's deposit experience applies verbatim to your branch today.

Practical Strategy: When GMS Fits — and When It Does Not

- Fit: 24K coins or bars sitting idle for five-plus years, no emotional wear value, you want modest yield and formal documentation.

- Maybe: Mixed 22K scrap accumulated from broken pieces — if melt loss is acceptable and tax records are clean.

- Poor fit: Bridal sets you may wear, gold you might pledge for emergency liquidity, or metal you plan to sell this year on the open market.

- Model interest plus locker savings minus melt loss before you sign — a 0.5% assay haircut on 200g is one full gram gone forever.

- If you need rupees within six months, a regulated gold loan may match your timeline better than locking metal in LTGD.

GMS Deposit Day: Documents and Preparation Checklist

| Item | Why the bank asks | Practical tip |

|---|---|---|

| PAN / Aadhaar KYC | Mandatory identity verification | Names must match across all IDs exactly |

| Proof of gold ownership | Purchase invoice or inheritance trail | Speeds audit if tax questions arise later |

| Bank account for interest | Interest credit destination | Use the account you file returns against |

| Separate stones (if any) | Only metal enters melt | Remove fittings before assay — stones are not deposited |

| Written deposit election form | STGD vs LTGD choice | Keep a signed copy; do not rely on verbal branch assurances |

Arrive with realistic time — assay and melt are not five-minute locker withdrawals. Ahmedabad branches may batch retail lots on specific weekdays; confirm the refinery courier schedule so you are not asked to leave metal overnight without a receipt. If the preliminary test suggests purity below scheme minimum, decide on the spot whether to abort rather than accept a sharply reduced credit — walking away with an unmelted bar beats a bad deposit.

NRI families returning to Gujarat sometimes ask whether imported bars qualify — eligibility depends on documentation and assay outcome, not origin alone. Keep customs and purchase paperwork aligned with the name on your KYC; mismatches delay credit even when fineness is fine.

Frequently Asked Questions

1. What is the minimum gold for the Gold Monetisation Scheme?

Banks and refineries set minimum lot sizes — often starting around 30 grams raw gold for retail deposits after assay, but verify with your participating branch. Smaller lots may be rejected or batched.

2. Can I deposit gold jewellery under GMS?

Yes, but it is typically melted and assayed. Stones are removed; making and design value are lost. Plain bars and coins are operationally simpler.

3. Is GMS interest taxable in India?

Interest earned is generally taxable under applicable Income Tax rules. Confirm treatment with a qualified tax professional and see our gold tax guide for broader context — one link only.

4. How is GMS different from a gold loan?

A gold loan gives you cash now against pledged jewellery you can reclaim after repayment. GMS pays interest on metal you deposit into the scheme — no immediate liquidity, different contract.

5. Do I get the same jewellery back at maturity?

Redemption is in gold of prescribed fineness and equivalent weight per certificate terms — not the same physical ornament you deposited. Treat GMS as a financial deposit, not a jewellery safe-keeping service.

6. Is GMS better than selling old gold?

Selling gives immediate rupees at market buy-back rates; GMS preserves gold exposure plus interest. Choose based on whether you need cash now or want to keep metal in the system — see sell-old-gold guide for sale math.

Data Sources and References

- Reserve Bank of India (RBI) — Gold Monetisation Scheme framework and notifications.

- Bureau of Indian Standards (BIS) — purity and hallmark standards for assayed deposits.

- World Gold Council — Indian household gold stock and recycling economics.

- London Bullion Market Association (LBMA) — international refining and fineness benchmarks.

- International Monetary Fund (IMF) — macro context for gold as a financial asset.

Conclusion

The gold monetisation scheme in India rewards households willing to move idle bars and coins from passive storage into the formal system — not families clinging to wearable heirlooms. Compare STGD and LTGD interest after assay loss, understand tax on interest, and separate the scheme clearly from gold loans and scrap sales before you melt a single gram.

If your locker holds only coins with no wedding plan, a branch call this week costs nothing. If it holds your grandmother's necklace, leave GMS on the shelf and close the godrej — some gold pays emotional dividends no interest rate matches.

Disclaimer: This article is for informational and educational purposes only. GMS terms, interest rates, and tax rules change; verify live bank circulars and consult a qualified financial professional before depositing.

Keywords: gold monetisation scheme India, GMS gold deposit, gold monetisation interest rate, idle gold earn interest India, short term gold deposit, long term gold deposit RBI, gold monetisation vs gold loan.