When a wedding deposit, school fee, or medical bill arrives before your salary credit, many Gujarat families reach for the locker instead of selling heirloom gold. A gold loan lets you unlock rupee liquidity while keeping the chain or bangle in your name — provided you understand loan-to-value (LTV), the true annual cost after fees, and what happens if you miss an instalment. This guide is for borrowers comparing counters in Ahmedabad, Surat, and Vadodara, not for traders speculating on MCX.

For buy-back math when you eventually sell unpledged scrap, see our sell old gold guide — one link only: pledged gold cannot be sold until the lender releases it. For hallmark verification before you pledge, see the gold jewellery scams guide. Check today's gold price today on GS24Live before you visit a branch.

Key Takeaways

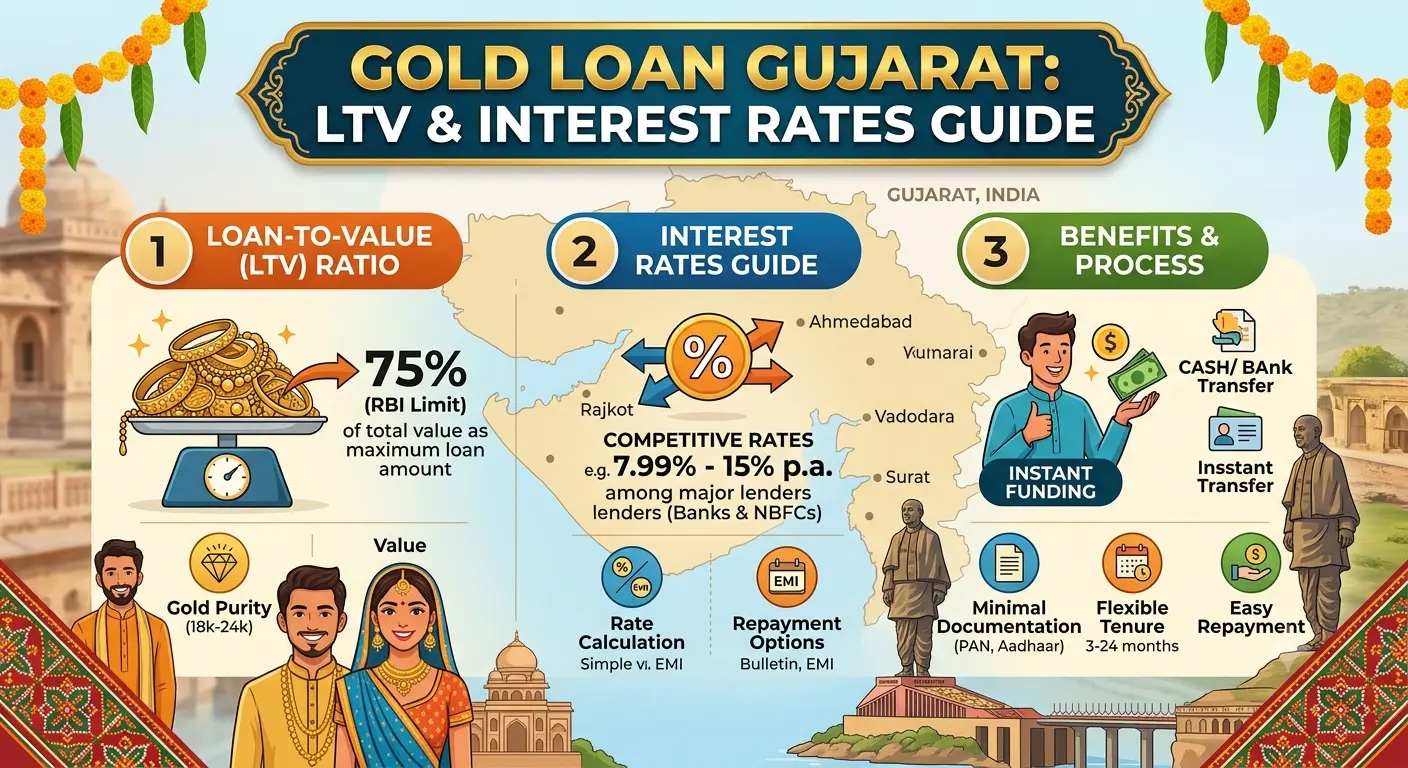

- RBI caps gold loan LTV at 75% of gold value on the sanction date — not 100% of your emotional estimate of the piece.

- Compare annual percentage cost: interest rate plus processing fee, appraisal charge, and late-payment penalties — not the headline "9% per annum" poster alone.

- Banks usually offer lower rates but stricter documentation; NBFCs and cooperative lenders may approve faster with slightly higher spreads.

- Never pledge without a printed sanction letter showing gross weight, net gold weight, purity, rate applied, and loan amount.

- Closure before selling scrap on the open market — lender rules apply first, not Manek Chowk morning boards.

What a Gold Loan Actually Is

You temporarily transfer physical gold to a regulated lender as collateral. The lender values the metal (usually 22K jewellery or 24K coins), applies the LTV cap, and credits rupees to your account. You retain ownership on paper; the packet sits in the lender's vault until you repay principal plus interest. Default beyond the grace period can trigger auction under the lender's policy — a very different outcome from a voluntary scrap sale.

Gold loans suit short-to-medium liquidity needs (3–24 months) when you intend to reclaim the jewellery. They are a poor substitute for long-term investment planning — for paper gold options, see our gold ETF guide in one sentence only.

How LTV Is Calculated on Your Jewellery

Loan-to-value is the rupee loan divided by the assessed gold value on sanction day. RBI guidelines limit how much lenders can advance against pledged gold. The assessment chain matters as much as the cap.

| Step | What the lender does | Effect on your loan |

|---|---|---|

| Gross weighing | Total piece on certified scale | Starting weight — not final collateral weight |

| Stone deduction | Non-gold mass removed from calculation | Lowers eligible metal weight on bridal sets |

| Purity test | Hallmark, HUID, or assay | 916 vs lower fineness changes value tier |

| Rate application | Internal gold rate on sanction date | Usually below retail sell rate |

| LTV application | Up to regulatory cap on assessed value | Final sanctioned loan amount |

Worked Example: 50-Gram 22K Chain (Illustrative)

| Line | Sample figure | Notes |

|---|---|---|

| Net gold weight | 50.0 g | Plain chain, no stones |

| Lender gold rate | ₹9,400 / g (22K sample) | Internal board, not showroom sell rate |

| Assessed gold value | ₹4,70,000 | 50 × 9,400 |

| LTV at 75% | ₹3,52,500 max loan | Regulatory ceiling — lender may offer less |

| Interest at 10% p.a. | ~₹2,938 / month (interest-only sample) | Actual EMI structure varies by product |

| Processing fee (1% sample) | ₹3,525 one-time | Often deducted upfront — raises true cost |

Always ask whether the processing fee is deducted from disbursement. A ₹3.5 lakh loan with ₹3,525 deducted upfront means you receive less cash while interest may still apply on the gross sanctioned amount.

Bank vs NBFC vs Cooperative: Lender Comparison

| Lender type | Typical interest band (illustrative) | Speed | Best for |

|---|---|---|---|

| Public sector bank | 8.5%–11% p.a. | Same-day to 2 days with full KYC | Lower rate, patient documentation |

| Private bank | 9%–12% p.a. | Often same-day in metro branches | Digital-savvy borrowers with salary account |

| NBFC gold loan | 11%–18% p.a. | Fast — sometimes under an hour | Urgent liquidity, simpler paperwork |

| Cooperative / local society | 9%–14% p.a. | Varies by district | Community trust, smaller ticket sizes |

Rates change with RBI policy and lender appetite — verify live numbers on the day you apply. For how repo moves affect bullion broadly, see our RBI repo rate and MCX gold guide — one sentence only; loan pricing follows a different transmission path than MCX futures.

Hidden Charges That Inflate the Real Cost

- Processing / appraisal fee: Flat or percentage — ask if refundable on early closure.

- Penal interest: Jumps after missed EMI or overdue interest — read the sanction letter footnotes.

- Part-release charges: Some lenders charge to return one bangle from a multi-piece packet.

- Auction-related costs: If you default, legal and auction fees may erode surplus after recovery.

- Insurance (optional): Premium for pledged gold cover — useful but adds to annual cost if bundled without choice.

The honest comparison metric is total rupees out over the planned tenure, not the lowest advertised rate on a highway billboard.

Documents and KYC Checklist

| Document | Why lenders ask | Tip |

|---|---|---|

| Aadhaar / PAN | Mandatory KYC | Carry originals and photocopies |

| Address proof | Regulatory requirement | Match Aadhaar address or carry valid alternate |

| Passport photo | Loan file | Two copies speeds rural branch processing |

| Prior gold invoice (if available) | Supports purity claim | Speeds assessment — not always mandatory |

| Bank account details | Disbursement | Confirm name match with KYC exactly |

Historical Gold Loan Growth in India

| Period | Market feature | Borrower impact |

|---|---|---|

| Pre-2014 | Fragmented pawnbrokers, weak transparency | High informal rates, poor documentation |

| 2014–2020 | NBFC gold loan chains expand | Faster sanction, printed packets, branch networks |

| 2021–2023 | Digital KYC and doorstep pickup in cities | Convenience rises; compare before doorstep premium |

| 2024–2026 | High gold prices lift collateral values | Higher absolute loans on same gram weight — do not over-borrow emotionally |

Ahmedabad, Surat & Rajkot: Where Gujarat Borrowers Shop for Rates

Gujarat's gold loan market splits by urgency and ticket size. Ahmedabad's CG Road and Ashram Road bank branches see salaried families pledging 22K sets before festival season. Surat's diamond-belt entrepreneurs often use NBFC same-day desks for working-capital gaps. Rajkot and smaller district towns rely on cooperative societies where relationship managers know repeat borrowers by name.

- Visit two lenders the same morning when MCX and local boards are stable — sanction rates are snapshotted on that day, not your memory of last month's peak.

- Ask Ahmedabad NBFC counters whether their internal gold rate matches the bank next door — a ₹200/gram assessment gap on 40 grams is ₹8,000 less loan for the same chain.

- Insist on photographing the sanction slip with gross weight, net weight, and rate before the packet leaves your sight — Gujarat borrowers who do this report fewer part-release disputes.

- If you plan to reclaim jewellery before Diwali, confirm partial prepayment rules upfront; some lenders charge for early closure within the first 90 days.

Risks When Pledging Family Gold Without Reading the Sanction Letter

Ornate bridal sets with heavy stone weight receive lower assessed value than plain chains — borrowers sometimes expect a loan based on gross showroom invoice from years ago. Default triggers auction timelines you cannot negotiate at Manek Chowk; the lender's policy governs. Co-borrower or guarantor clauses can affect family credit files if payments slip.

Never pledge entire family holdings in one packet if you only need partial liquidity — split loans where the lender allows, so one missed cycle does not put all heirloom pieces at auction risk.

Practical Strategy: Borrow Less, Exit Clean

- Borrow the minimum rupees needed — LTV headroom is not a target.

- Compare two lenders' all-in cost for your exact tenure, not just the rate poster.

- Set a calendar reminder three days before each interest due date — penal rates erase rate-shopping gains fast.

- Plan closure before any open-market scrap sale; lender release precedes Manek Chowk quotes.

- Store the sanction letter, packet receipt, and release certificate in the same folder as your HUID photos.

Frequently Asked Questions

1. What is the maximum gold loan I can get in Gujarat?

Lenders apply RBI's LTV cap against assessed gold value on sanction day — typically up to 75% of that value. Your net loan depends on weight, purity, stone deductions, and the lender's internal rate, not the showroom price tag on your invoice.

2. Is NBFC gold loan faster than a bank?

Often yes for small tickets with complete KYC — some NBFC desks sanction within an hour. Banks may offer lower interest but take longer on first-time files. Compare all-in cost, not speed alone.

3. What happens if I miss a gold loan payment?

Penal interest applies after the grace period in your sanction letter. Sustained default can lead to auction of pledged gold under lender policy. Contact the branch before missing — many offer restructuring if you engage early.

4. Can I sell pledged gold on the open market?

No. You must close the loan and receive the lender's release certificate before selling scrap or exchanging at a jeweller. Compare closure statement vs open-market sale using our sell-old-gold guide after release.

5. Are gold loan interest rates fixed or floating?

Most retail gold loans in India are fixed for the agreed tenure at sanction. Confirm whether your product allows mid-term rate revision on rollover — terms vary by lender.

6. Do I need a PAN card for a gold loan in Gujarat?

PAN is standard KYC for regulated lenders. Some cooperative societies accept Form 60 for smaller tickets without PAN — ask before you travel to the branch with incomplete documents.

Data Sources and References

- Reserve Bank of India (RBI) — gold loan LTV norms, NBFC regulation, and consumer credit framework.

- Bureau of Indian Standards (BIS) — hallmarking and purity assessment standards for pledged jewellery.

- Multi Commodity Exchange of India (MCX) — benchmark gold pricing context for lender rate boards.

- World Gold Council — Indian household gold ownership and liquidity behaviour.

- Reuters — bullion market news affecting collateral valuations.

Conclusion

A gold loan in Gujarat works when you treat it as a timed bridge — borrow the minimum, read the sanction letter for LTV and fees, compare bank and NBFC all-in cost the same morning, and plan a clean closure before any scrap sale. The jewellery stays yours only if repayments stay on schedule; hidden charges and penal interest turn a cheap headline rate into an expensive year.

Before you pledge, run the worked example against your own net weight, photograph the scale reading, and visit two lenders. That ten-minute discipline protects more family wealth than chasing an extra ₹5,000 on the sanctioned amount.

Disclaimer: This article is for informational and educational purposes only. Gold loans involve credit and collateral risks. Rates and LTV rules change; verify live terms with your lender and consult a qualified financial professional before borrowing.

Keywords: gold loan Gujarat, gold loan interest rate India, LTV gold loan, gold loan Ahmedabad, NBFC gold loan vs bank, gold loan hidden charges, pledge gold jewellery India.